The Trump Administration’s torrent of ever-changing tariff proposals, threats, and actions made 2025 an almost dizzying year for U.S. trade policy.

Despite the persistent uncertainty for U.S. businesses and high levels of import tax collections on American consumers (or “record-breaking tariff revenue,” as those in the Administration might say), the U.S. economy has remained resilient and even surpassed expectations in a few areas.

This resilience has led to critiques that many economists’ predictions about the impact of tariffs on growth and inflation fell flat. After all, the United States has not entered the recession many financial institutions warned about. This characterization of economic projections, however, fails to note that predictions changed constantly throughout 2025 alongside the Administration’s numerous trade policy shifts.

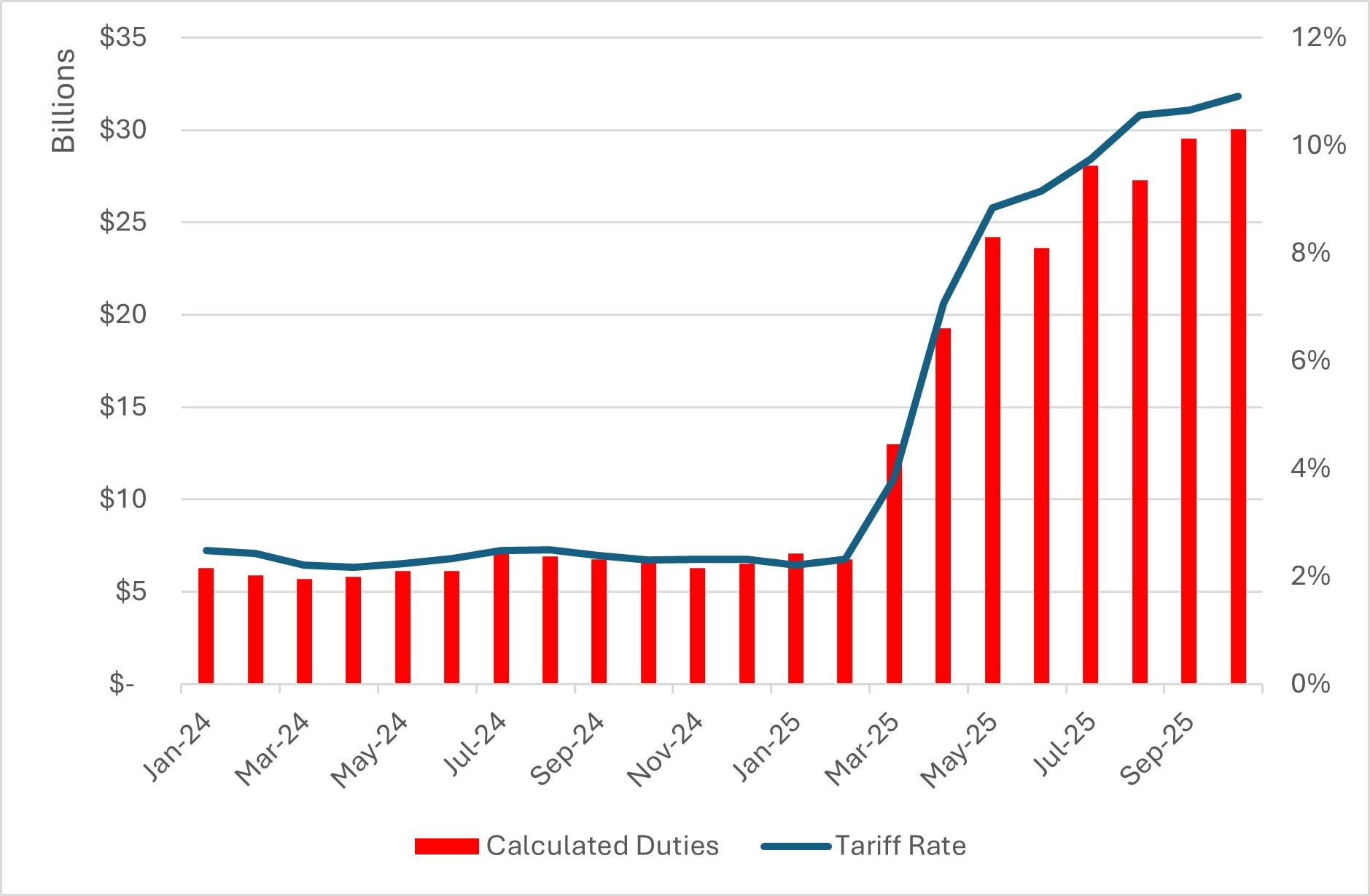

The tariff outlook has drastically changed over the past year, with the effective tariff rate skyrocketing from under 3 percent before President Trump’s inauguration to 28 percent post “Liberation Day.” It now sits at roughly 14 to 16 percent. The decline from the peak is due primarily to the pause of “Liberation Day” tariffs, which allowed for trade deals that solidified less drastic yet still elevated tariff rates.

The tariff outlook has drastically changed over the past year, with the effective tariff rate skyrocketing from under 3 percent before President Trump’s inauguration to 28 percent post “Liberation Day.” It now sits at roughly 14 to 16 percent.

The end of the trade war with China – which threatened tariffs over 145 percent – alongside a few tariff exemptions for food products, semiconductors, and other imports, has also eased tariff burdens. Each of these trade policy alterations has caused tariff collection estimates, gross domestic product (GDP) growth projections, and household cost estimates to shift.

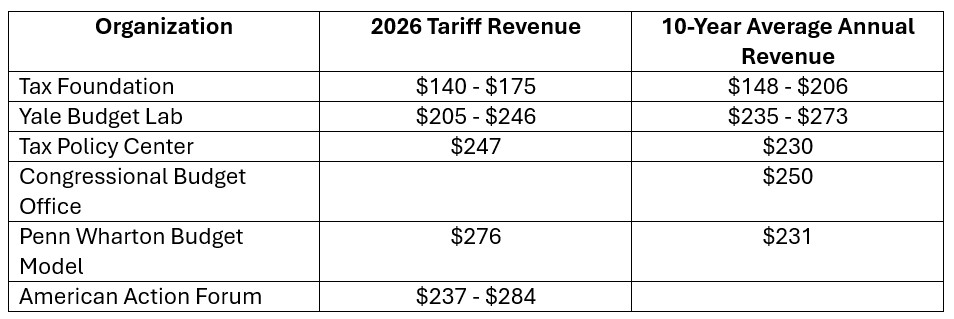

The day after “Liberation Day,” American Action Forum research put total annualized tariff costs at $366.5–391.6 billion. As of February 2026, this estimate sits around $237 billion. Factoring in other tariffs and proposals, this cost estimate approaches $284 billion annually, which is in line with the Bipartisan Policy Center’s current tariff tracker. Other tariff revenue estimates are included below in Figure 2.

Despite the range of estimates, there is consensus that U.S. businesses and consumers bear the vast majority of tariffs and that 2026 will continue to see upward pressure on consumer prices as businesses pass on more costs. A recent study found that 96 percent of the tariff burden is being absorbed by U.S. businesses and consumers rather than foreign exporters, supporting past research from both The Budget Lab at Yale and the Harvard Business School. This means that U.S. taxes increased to the tune of $200 billion in 2025, counteracting the Trump Administration’s pro-growth deregulatory agenda and tax cuts. Furthemore, 2025’s relatively mild inflationary figures are not indicative of tariffs having mild economic impacts, but instead point to other factors dampening their potency, such as low oil prices, higher productivity, and the gradual passthrough of tariff costs to consumers.

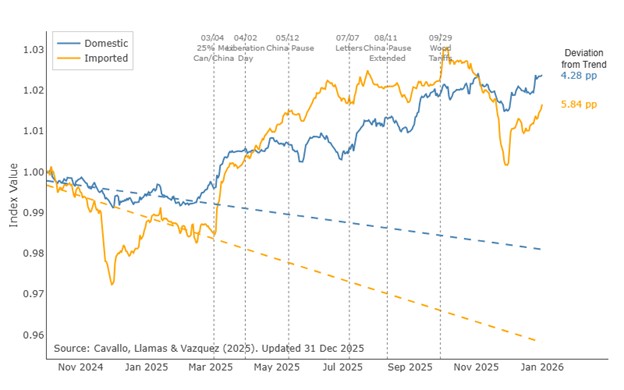

The tariff tax hike has had noticeable economic effects. First, tariffs reversed the downward trend in inflation for many goods categories, with the consumer price index remaining well above the 2-percent target. In fact, year-over-year inflation had declined from 3–2.3 percent between January and April last year but has since risen to 2.7 percent as of December. Additionally, four major retailers’ inflation trends were upended in the aftermath of tariff implementation as tracked by the Pricing Lab at Harvard in Figure 3. As a result, consumer spending on categories directly impacted by tariffs either stabilized or fell.

A recent study found that 96 percent of the tariff burden is being absorbed by U.S. businesses and consumers rather than foreign exporters. This means that U.S. taxes increased to the tune of $200 billion in 2025.

Second, U.S. economic growth projections contracted since January 2025 in response to the shifting trade landscape. According to the Congressional Budget Office, real GDP growth projections for 2025 decreased from 1.9 percent in January to 1.4 percent in September, although 2026 estimates have increased from 1.8–2.2 percent. Notably, U.S. economic growth – at least in the first half of 2025 – is being increasingly driven by the artificial intelligence data center buildout and high-tech spending. The World Economic Forum estimates that 80 percent of the increase in final private domestic demand came from these two drivers.

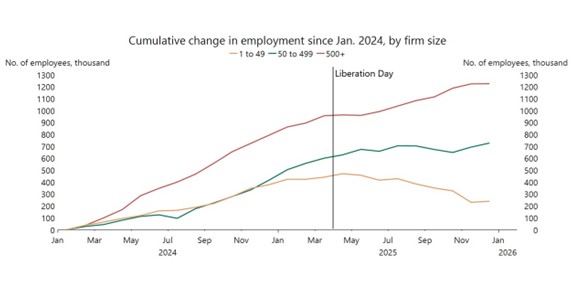

Finally, there are signs that additional tariff costs passed onto U.S. businesses have resulted in a weaker labor market, especially for small businesses. Since “Liberation Day,” U.S. employment growth among small businesses has underperformed large businesses (Figure 4). Employment in firms with 1-19 employees fell by 62,000 while employment in firms with 20-49 employees fell by 122,000 throughout 2025, potentially as a result of cost-cutting measures. There are numerous reasons why small businesses are at a disadvantage in dealing with higher tariffs, one being they tend to have far more concentrated supply chains. Most small businesses rely on just one supplier and import a select few products, which prevents them from easily adjusting to changing tariff policies like larger firms that import from 50 or more countries.

One recommendation for the Trump Administration would be to avoid conflating positive economic reports with tariff policy success. In many instances, tariffs have dampened the overall economic growth effects that stem from tax reductions and reduced regulatory burdens. It is in fact possible to achieve beneficial trade and investment agreements with other countries without maintaining burdensome import taxes. Lowering the effective tariff rate would remove much of the economic headwinds that are counteracting pro-growth policies.

At the very least, establishing greater certainty on the future of tariff policy is vital for businesses to plan accordingly. Furthermore, the constitutional authority to levy taxes lies in the hands of the legislative branch. If Congress has something to say about the negative consequences of tariffs, then it is time to legislate on the issue.

Jacob Jensen is the Trade Policy Analyst at the American Action Forum.