The United States celebrates its 250th birthday confronting an extraordinary threat. Rather than a war against an aggressive foreign adversary, the nation has spent several decades inflicting this threat on itself, even as experts warned that we were heading toward what a former presidential chief of staff called “the most predictable economic crisis in history.”

I’m referring to the rapidly escalating federal debt, which is already slowing the economy, pushing up inflation and interest rates, and squeezing key spending priorities. This path leads toward a debt crisis followed by dramatic, painful tax increases.

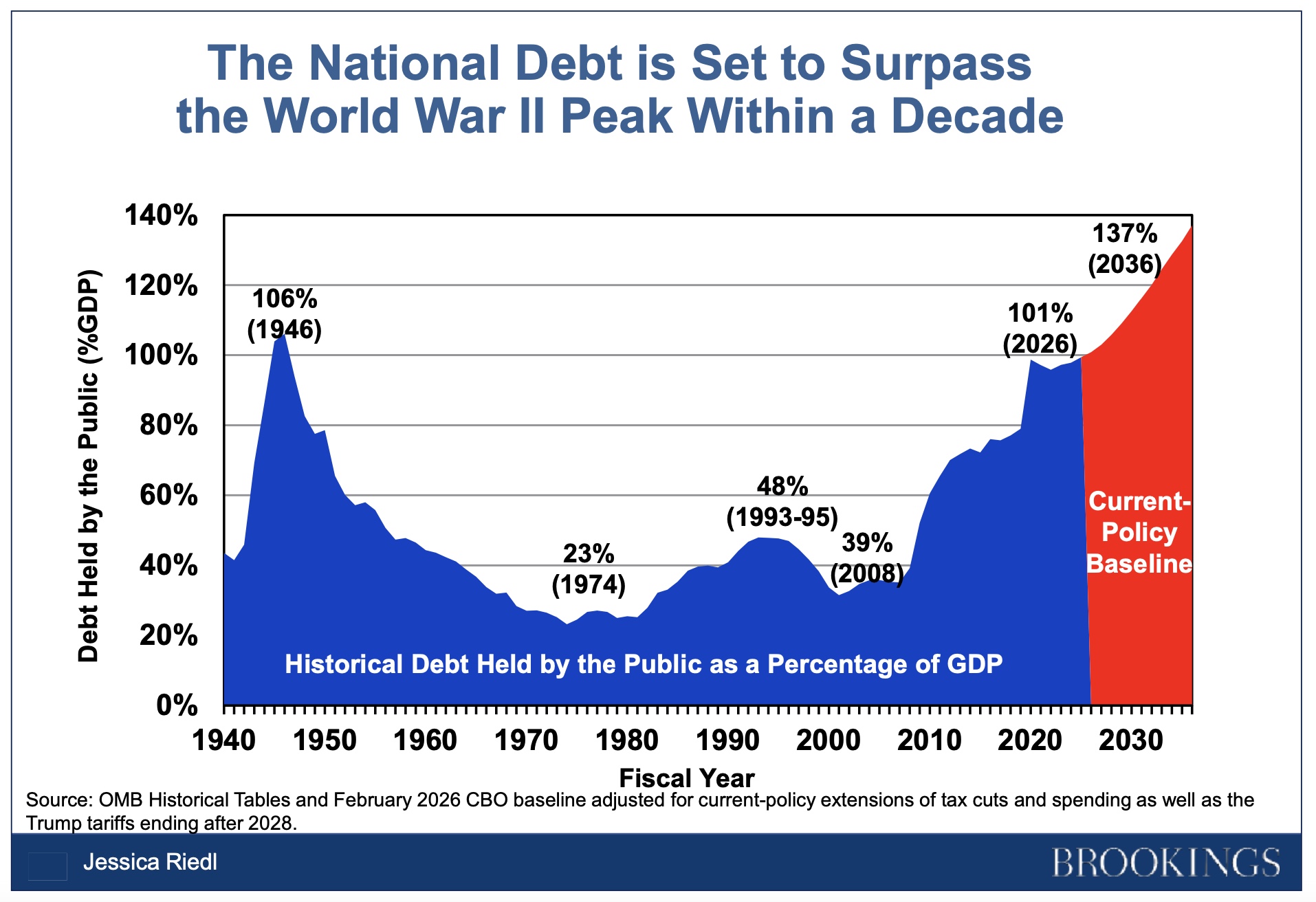

Americans have often run up debt during wars and emergencies, knowing the burden could be reduced once the crisis passed. The American Revolution, Civil War, and World War I each pushed the federal debt to roughly 30 percent of GDP. Yet the end of those wars returned the nation to normalcy and brought sharp reductions in the debt’s share of the economy — the country even retired it entirely, if briefly, in the 1830s. After World War II pushed the debt to a staggering 106 percent of the economy, small annual deficits and rapid economic growth brought that share down to 23 percent by the mid-1970s. Washington even ran budget surpluses between 1998 and 2001.

That era has ended. Since 2008, the federal debt has leaped from 40 to 100 percent of the economy — nearly matching the World War II peak. Aggressive federal responses to the Great Recession and, especially, the Covid pandemic drove much of this debt. Yet Americans also simply stopped caring about deficits, demanding endless tax cuts and spending expansions that have handed the U.S. the largest budget deficits among the 38 OECD nations. Today, annual deficits of nearly $2 trillion—in an era of relative peace and prosperity — elicit yawns from most policymakers and voters.

Since 2008, the federal debt has leaped from 40 to 100 percent of the economy—nearly matching the World War II peak.

And the fiscal outlook is only growing more daunting. Simply extending current policies would drive the debt past 240 percent of the economy within three decades. Soaring interest costs are projected to consume nearly one-third of all federal taxes within a decade, and between 54 and 83 percent — depending on interest rates — within three decades.

Past wars and economic crises were expensive but temporary, and lawmakers and voters made sure to return to fiscal responsibility afterward. Today’s surging deficits are driven by our insatiable appetite for European-style government benefits at low tax rates. Never before have Americans run up so much debt in peacetime while caring so little.

Sure, voters tell pollsters they would prefer smaller deficits—right after their elected officials finish cutting their taxes and expanding their benefits. When pressed, many cling to hyper-partisan myths that blame the deficit entirely on their favorite political targets. Liberals blame tax cuts for the rich and “forever wars.” Conservatives blame immigrants, foreign aid, and fraud. Those costs are real but relatively minor contributors to deficits projected to reach $200 trillion over three decades. Our deficits result primarily from Social Security and Medicare, which face a 30-year cash shortfall of $157 trillion. And we keep demanding tax relief, even as the median-earning family now pays an effective federal income tax rate of just 2 percent.

Today’s surging deficits are driven by our insatiable appetite for European-style government benefits at 1790s tax rates. Never before have Americans run up so much debt in peacetime while caring so little.

Bloated deficits are already harming the economy, as described above. But the real danger arrives when the bond market can no longer keep up with Washington’s demand for $200 trillion in new borrowing over the next three decades. At some point, an overextended bond market will demand much higher interest rates, driving up federal interest costs and then borrowing costs across the government and economy in a vicious cycle. No one knows exactly when the bond market will tap out—but we are likely to find out unless we reverse course.

Calling this merely fiscal irresponsibility misses the point. It is an abdication of generational responsibility. In the greatest intergenerational wealth transfer in history, seniors are dumping a $157 trillion Social Security and Medicare shortfall onto today’s young people. Washington already spends six times as much on seniors as on those under 26, and that gap will only widen. Future taxpayers, meanwhile, will surrender half their federal taxes just to cover interest on this inherited debt. And much of that burden exists to guarantee (even wealthy) seniors benefits far exceeding what they paid into Social Security and Medicare.

America’s only way out is for us to finally get serious and stop demanding free lunches from the government. That requires putting all spending and taxes on the table, while recognizing that most savings must come from the Social Security and Medicare shortfalls driving the bulk of the debt. After all, drowning today’s young people in taxes is no better than drowning them in debt. Americans have long been willing to sacrifice for their children, their grandchildren, and the future of America. Today, that doesn’t mean fighting a war; it simply means living within our means.

Jessica Riedl is a fellow at the Brookings Institution. Follow her on Twitter @JessicaBRiedl.