America’s business leaders have long warned that the outdated, inefficient and anti-competitive U.S. tax system is threatening the shared prosperity that our nation’s citizens should be able to count on.

Thankfully, more and more people of both political parties understand this threat. Leading members of Congress are working on promising new reform plans that could fix the many flaws of the U.S. tax code and, in the process, counteract years of lagging growth and employment.

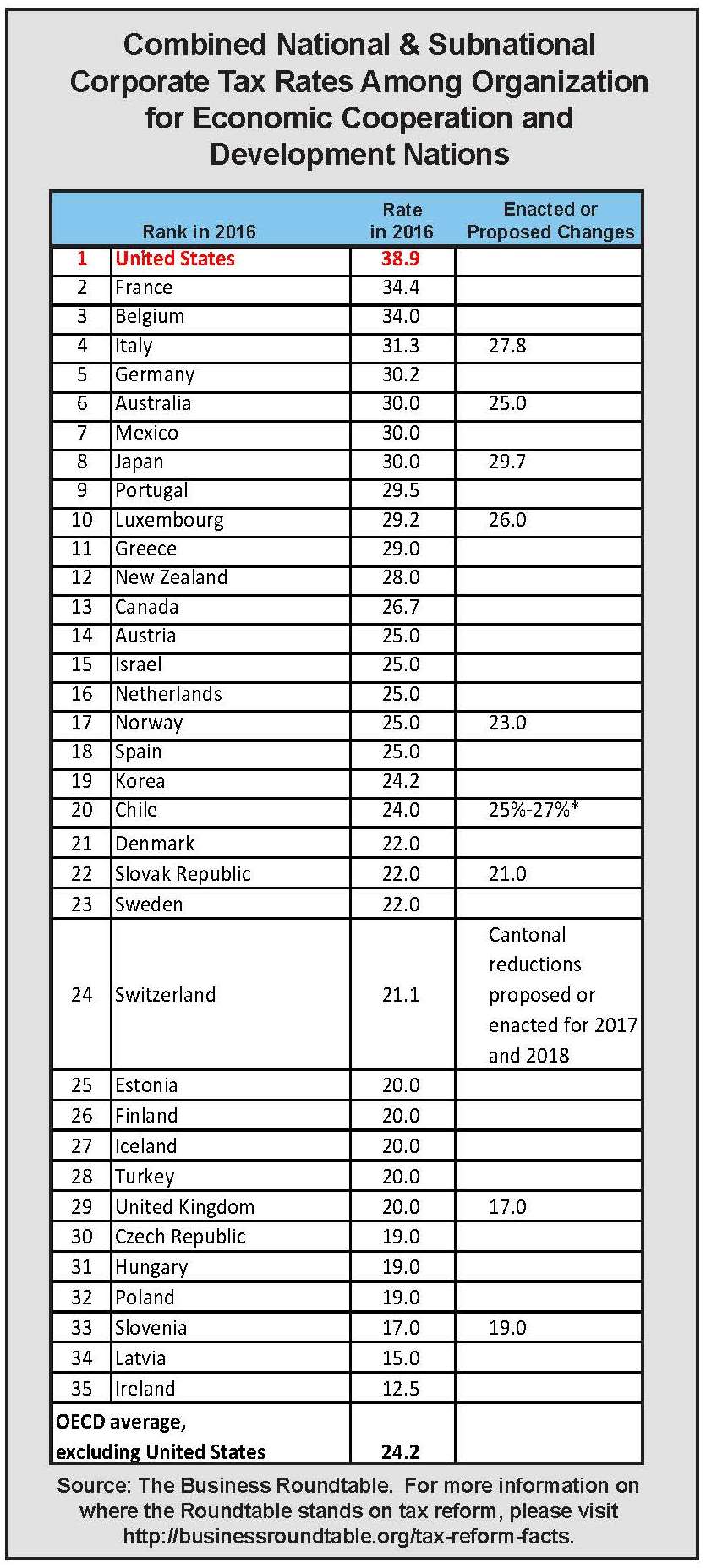

While comprehensive reform of the tax code is needed, two problems are especially problematic for business and harmful to the U.S. economy: 1) the high corporate tax rate – now 40 percent, including state and local taxes – the highest in the developed world; and, 2) our nation’s policy on taxation of income earned outside the U.S.

Three decades ago, when President Reagan signed the Tax Reform Act of 1986 into law, the corporate tax rate was among the lowest in the world. Other countries took note. They began dropping their rates and improving their tax systems. This has been especially true over the last ten years – a period that not only saw the U.S. statutory corporate income tax rate remain steady, but saw a plethora of foreign countries create sophisticated tax systems and drop their rates below U.S. levels.

Three decades ago, when President Reagan signed the Tax Reform Act of 1986 into law, the corporate tax rate was among the lowest in the world. Other countries took note.

Why does this matter? The Organization for Economic Cooperation and Development (OECD) has reported that, “Corporate income taxes are the most harmful for growth as they discourage the activities of firms that are most important for growth: investment in capital and productivity improvements.”

The United States is the only major country that taxes worldwide income, an outmoded approach that our competitors have abandoned to create a more welcoming environment for investment.

Other countries tax only earnings made in their country, enabling companies based there to readily send money they earned abroad back home. In contrast, the United States adds its own domestic corporate taxes when a company seeks to return profits home.

“Consequently, foreign companies can afford to bid more for acquisitions in the United States and abroad as compared to U.S. companies,” concluded the global consulting firm EY in a 2015 report on cross-border mergers and acquisitions (M&A). As a result, the U.S. economy has lost $179 billion in assets over the last 10 years.

Overwhelmingly, the U.S. companies being acquired by foreign entities represent smaller scale, newer companies – the kind that innovate and grow, fostering a dynamic economy that puts people to work. As EY’s study put it, “Divesting some lines of business and acquiring others allows companies to enter new markets, access distribution channels, develop new technologies, and release capital for reinvestment.”

Put simply, a high corporate tax rate and our self-defeating method of taxing income earned outside the U.S. have slowed our economic growth, made it harder for our companies to compete in the international marketplace, and made it easier for our companies to be bought by foreign competitors. Moreover, these policies are a major disincentive to establishing corporate headquarters in the U.S. As a result, we’ve lost up to 1300 companies in the U.S. over the last ten years – innovators that would have been spinning off their ideas for the benefit of U.S. workers and consumers. With our lagging GDP, we could use those companies and the jobs they create!

A high corporate tax rate and our self-defeating method of taxing income earned outside the U.S. have slowed our economic growth.

The consequences to U.S. workers should not be underestimated. One study cited by the House Ways and Means Committee reported that the failure of the United States to keep our corporate rate competitive with other countries reduces wages by 1.0 to 1.2 percent.

Recognition of the problem is also bipartisan. Laura Tyson, the former top economic advisor to President Bill Clinton, said that: “For many years, the conventional wisdom was that the corporate income tax was principally borne by the owners of capital in the form of lower returns. Now, with more mobile capital, workers are bearing more of the burden in the form of lower wages and productivity as investments move around the world in search of better tax treatment and higher returns.”

The impact on employees, businesses and the economy is why American business leaders were encouraged by the recent work done on tax reform by Chairman Kevin Brady (R-TX) of the Ways and Means Committee. In June, Chairman Brady and Speaker Paul Ryan (R-WI) unveiled a tax reform blueprint that could spur much-needed change in 2017.

The Chair of the Business Roundtable Tax and Fiscal Policy Committee said the blueprint contained provisions that could “dramatically improve” the U.S. investment climate for both domestic and foreign businesses.

“Competitive business tax rates and a modernized international tax system are needed to add jobs, boost wages and grow the economy,” said Mark Weinberger, Chairman and CEO of EY.

The current economic recovery is the weakest since the post-WWII era, with annual GDP growth never topping 3 percent since the end of the Great Recession – an unprecedented period of slow growth that has also witnessed millions of people giving up on work altogether.

Business leaders agree that modernizing our tax code through major tax reform is the best way to escape this rut and expand growth, encouraging innovation and investment, hiring and improved wages. Congress and the next President should make reform a priority in 2017.

John Engler serves as President of the Business Roundtable. A former three-term governor of Michigan, he previously served as President & CEO of the National Association of Manufacturers. For more information on where the Business Roundtable stands on tax reform, please visit http://businessroundtable.org/tax-reform-facts.